CSDR: promising signs from the new settlement discipline regime

Cash penalties introduced under the Settlement Discipline Regime (SDR) are working, early data and anecdotal evidence show. With market participants already incentivized to get their post-trade in order, we argue that mandatory buy-ins could introduce fresh risks into the process.

Following several delays, a new framework for settling securities transactions came into force on Feb. 1. A core element of the European Union’s Central Securities Depositories Regulation (CSDR), the Settlement Discipline Regime (SDR) creates measures to help buyers and sellers settle securities transactions safely and on time. Among the new obligations are cash penalties for market participants who cause fails, as well as various monitoring and reporting commitments.

The SDR went into effect without one of its more controversial measures: mandatory buy-ins. This provision, dropped at the last moment1, would have penalised sellers who fail to deliver securities on time by making it compulsory for purchasing parties to initiate a buy-in process against the seller.

Instead of scrapping mandatory buy-ins altogether, the European Commission has issued a new legislative proposal to make buy-ins enforceable at the discretion of authorities. Specifically, regulators would have the right to push through mandatory buy-ins for specific asset classes or product categories if cash penalties haven’t caused long-term improvements in settlement rates, rates are below comparable jurisdictions, or if the level of fails impacts financial stability.

While we welcome more clarity on mandatory buy-ins, we also feel it’s worth stepping back and assessing the early impact of the legislation. Nearly two months of data and anecdotal findings suggest cash penalties are working. By introducing fresh risks into the post-settlement process, we feel there’s a danger that mandatory buy-ins could undermine the very goals of SDR.

Positive Signs

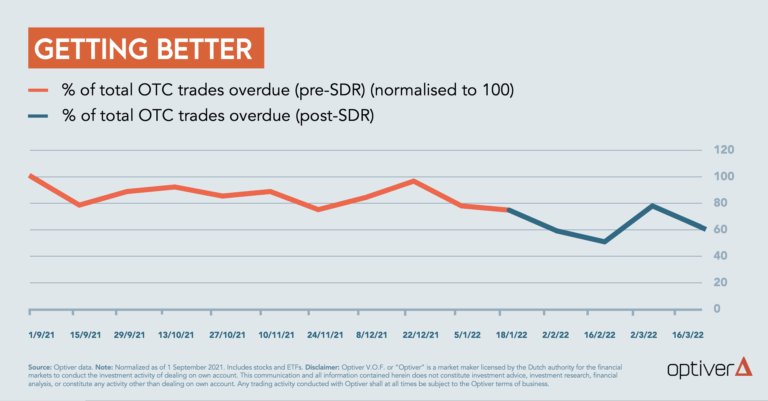

The proportion of overdue OTC trades in stocks and exchange-traded funds has dropped since SDR came into effect, even accounting for March’s market volatility (see chart). There is now strong incentive for participants to get their post-trade in order. Over time we expect this trend to continue due to the rules-based nature of matching and settlement. Optiver has been able to automate much of the post-trade process, and we expect the rest of the market to be able to do the same.

Anecdotal findings confirm what the data show. After go-live, market participants have put more focus on post-trade processes such as trade confirmations. Those wishing to avoid penalties are also more considerate to proper post-trade communication. In particular we have observed the following:

- Trade confirmations are sent in a more timely fashion;

- Much higher response rate to issue escalation; and

- Significant improvement in matching performance, including better follow-up.

Post-trade communication tools are improving in ways that allow for early detection of problems in the trade life cycle. They’re also leveling the playing field between buyside and sellside market participants.

One example comes from a trade confirmation and allocation service popular with large financial institutions. Prior to SDR go-live, the place of settlement – a critical component in the settlement matching process – wasn’t a required field in trade confirmations. It’s now a mandatory field that must match between buyer and seller. Removing this ambiguity has increased certainty and led to fewer disputes, creating a smoother post-trade process.

We have also observed that market participants are including more complete trade confirmations in post-trade communications. Apart from the ‘usual’ trade financials (such as security identifiers, price, size, trade and settlement date), market participants have made critical information more explicit, such as the place of settlement and the settlement account details, in order to avoid hold-ups that could result in penalties.

Looking Ahead

In our view cash penalties are working to inject more order into the post-trade process. And while adapting to the new rules has in some cases required additional outlay from firms, over time fewer resources should be required to handle matching and settlement. This in turn will increase market efficiency, one of the stated goals of SDR.

Mandatory buy-ins – whether compulsory or not – could disrupt this progress by introducing additional risk into the post-trade process. Existing trades might need to be cancelled, new trades would need to be done, and new participants would need to be found. We feel that in many cases, the additional risks of a buy-in process would be disproportionate.

Mandatory buy-ins also disrupt dividends and corporate actions, as well as securities lending and repo markets. In order to account for the risk of mandatory buy-ins, lenders are likely to raise costs or withdraw inventory altogether. For market-makers, this could raise the costs of managing risks via short positions, which could have a negative impact on liquidity. Mandatory buy-ins also introduce an additional operational burden from the associated costs of implementation.

Finally, we wonder whether looking at settlement rates in comparable jurisdictions is the best way of deciding whether to impose buy-ins. The European settlement landscape remains somewhat fragmented across national lines. Some post-trade barriers – already identified around the time of the introduction of the Euro – still remain. As a result, Europe today has several dominant national systems. That makes it unique compared with the U.S., for example, where all stocks settle in one system. In our view, comparative settlement rates wouldn’t be an accurate measure of the relative effectiveness of the existing settlement regime.

A well-functioning and reliable post-trade process is critically important for the functioning of markets. With early evidence suggesting that cash penalties are working, we feel authorities should wait and see before introducing additional risk in the form of buy-ins.

1 https://www.esma.europa.eu/press-news/esma-news/esma-calls-deprioritise-buy-in-supervision

Optiver supports open discussion and debate on all market structure topics that would lead to an improvement of the market.

To discuss this paper – or any other market structure topic – reach out to the Optiver Corporate Strategy team at [email protected]

DISCLAIMER: Optiver V.O.F. or “Optiver” is a market maker licensed by the Dutch authority for the financial markets to conduct the investment activity of dealing on own account. This communication and all information contained herein does not constitute investment advice, investment research, financial analysis, or constitute any activity other than dealing on own account.