A better way to measure best execution

Regulators have suspended RTS 27 reporting and are considering scrapping the requirement to produce RTS 27 and RTS 28 reports altogether. These reports are designed to show the extent to which investors in the U.K. and EU receive best execution for their trades, and they do have some issues in their current form. Instead of eliminating them altogether however, we advocate for making them more useful and less cumbersome to produce. For more on best execution and related topics, see Further Reading.

Regulators in the U.K. and EU recently suspended the requirement that trading venues produce RTS 27 reports and are considering scrapping the requirement to produce RTS 27 and RTS 28 reports altogether. These reports were designed to ensure that brokers and trading venues provide “best execution.”

While no doubt designed with the best of intentions, market participants say they’re confusing and filled with redundant information, particularly in light of the cost and effort they take to produce. While we’re strongly in favor of promoting transparency in trade data, we do feel these reports have shortcomings in their current form. But instead of doing away with them, why not change them to present more useful information in a clearer way?

Here are some ideas for how to go about this improvement.

Background

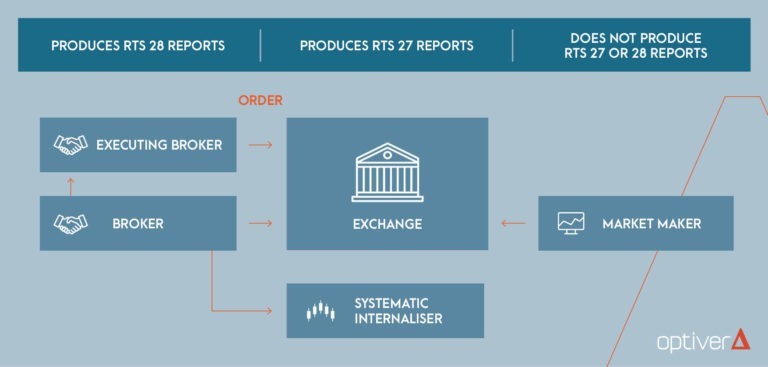

Introduced under the MiFID II legislation, best execution requires brokers to take all reasonable steps to get the best possible result for their clients when it comes to executing their trades (taking into account things like price, cost, speed and likelihood of execution). RTS 27 and 28 reports are a key way market participants verify whether investors are getting best execution. Trading venues produce RTS 27 reports, while RTS 28 reports are generated by brokers.

RTS 27

Overall, we favor simpler disclosure in RTS 27 reports. Market participants should get a clear idea from the reports of how much a particular instrument trades on a given venue. The reports should provide a sense of whether they’re missing out on important sources of liquidity if they’re not routing to these venues. It should also complement the benchmarking they already do for venues they connect to, deepening their analysis of whether best execution is being achieved.

We agree with the general consensus that much of what’s disclosed in RTS 27 reports is unnecessary and uninformative. For instance, a recent AFME/Oxera report found 540 different ways to tag trades that happen over-the-counter or in systematic internalizers, which strikes us as too many. Trade types in these reports should be standardized and simplified. There are already industry standards in place that could be used here.1

We note that current RTS 27 reports are very data-intensive, making them accessible to those with data analysis skills but not necessarily to your average person. To broaden the audience for these reports, we favor including an “executive summary”. What is key is that there be an industry-wide standard, which would remove a lot of the data analysis work, but also the judgment calls that can crop up when attempting to interpret a report. It would also make it easier to compare reports across venues and possibly also join them up with the related RTS 28 reports. That said, it’s important to ensure that market participants still have access to the detailed underlying data. A lot of the useful nuance and ability to compare venues in detail would be lost if the only thing available is a high-level report.

To the extent that European regulators are willing to look abroad, there is potentially a lot of value in replicating the Rule 605 reports that are required in the U.S. Similar disclosures would also reduce the burden for many global firms that already produce Rule 605 reports. They could use the same infrastructure to generate their RTS 27 reports.

RTS 28

We believe that RTS 28 reports in their current form largely fulfill their remit, which is to provide basic clarity on where brokers route their orders. These reports can quickly highlight cases where brokers rely on very few venues (especially SI or OTC venues) or affiliated entities for the bulk of or entirety of their execution – both red flags for potential conflicts of interest.

But we think a few extra sections would make these reports a lot more useful (and at little additional cost). For instance, we would propose adding a section highlighting how much flow brokers route to affiliated entities or SIs for execution, regardless of whether those entities falls into the top 5 in any of the current categories. That would clearly flag areas of potential conflicts of interest that come from internal routing.

Also useful would be additional disclosure that shows how much brokers receive in compensation (if any) for their flow per destination. Again, the idea here is to highlight potential conflicts of interest that can arise with payment for order flow or similar arrangements, which remain legally ambiguous across the EU.

RTS 28 reports would be more useful if they were published more quickly and with greater frequency. Why not implement a quarterly publication schedule, alongside the RTS 27 reports, with a shorter timeline between end of year/quarter and publication? As with the RTS 27 reports, regulators should create a standardized format for the RTS 28 and make them easier to find for any broker. Ideally, they would be accessible in a central location such as the ESMA register, as well as on individual brokers’ websites.

Alongside human-friendly PDFs, we believe the data should be presented in a machine readable format (such as csv) so that data analysts can analyze a large volume of reports together. One advantage of a machine readable format is that it could easily include all routing destinations, not just the top five.

Finally, it would be beneficial to extend RTS 28 reports to cover situations where brokers route orders to other brokers. Currently, RTS 28 reports show only the next step in the chain (i.e. the broker to whom the flow has been routed, but not where that broker ends up executing). The best way to judge execution quality is to look at the venue where the order is ultimately traded however, and how competitive that venue is in terms of both fees and spreads.

Conclusion

We recognize that producing these reports comes at a cost and, as with any regulation, that cost must be weighed against the value the reports provide. We do agree with the general consensus that the current RTS 27 and 28 reports do not provide the insight they are meant to provide. With the proper implementation, these reports can stimulate competition and highlight possible conflicts of interest, resulting in better outcomes for investors large and small. Rather than scrapping them entirely, we propose a series of changes that should increase their value while also reducing the effort and cost involved with producing them (especially in the case of RTS 27).

Further Reading

- ESMA statement related to suspension of RTS 27 reports.

- ESMA market consultation on best execution reports.

- Explainer about MiFID II’s best execution requirements.

- Background on Rule 605 reports.

Optiver supports open discussion and debate on all market structure topics that would lead to an improvement of the market.

To discuss this paper – or any other market structure topic – reach out to the Optiver Corporate Strategy team at [email protected]

DISCLAIMER: Optiver V.O.F. or “Optiver” is a market maker licensed by the Dutch authority for the financial markets to conduct the investment activity of dealing on own account. This communication and all information contained herein does not constitute investment advice, investment research, financial analysis, or constitute any activity other than dealing on own account.

[1] FIX’s Market Model Typology, for instance, could serve the very same purpose here.